The Napkin Math Retirement Plan (Stop Overcomplicating It)

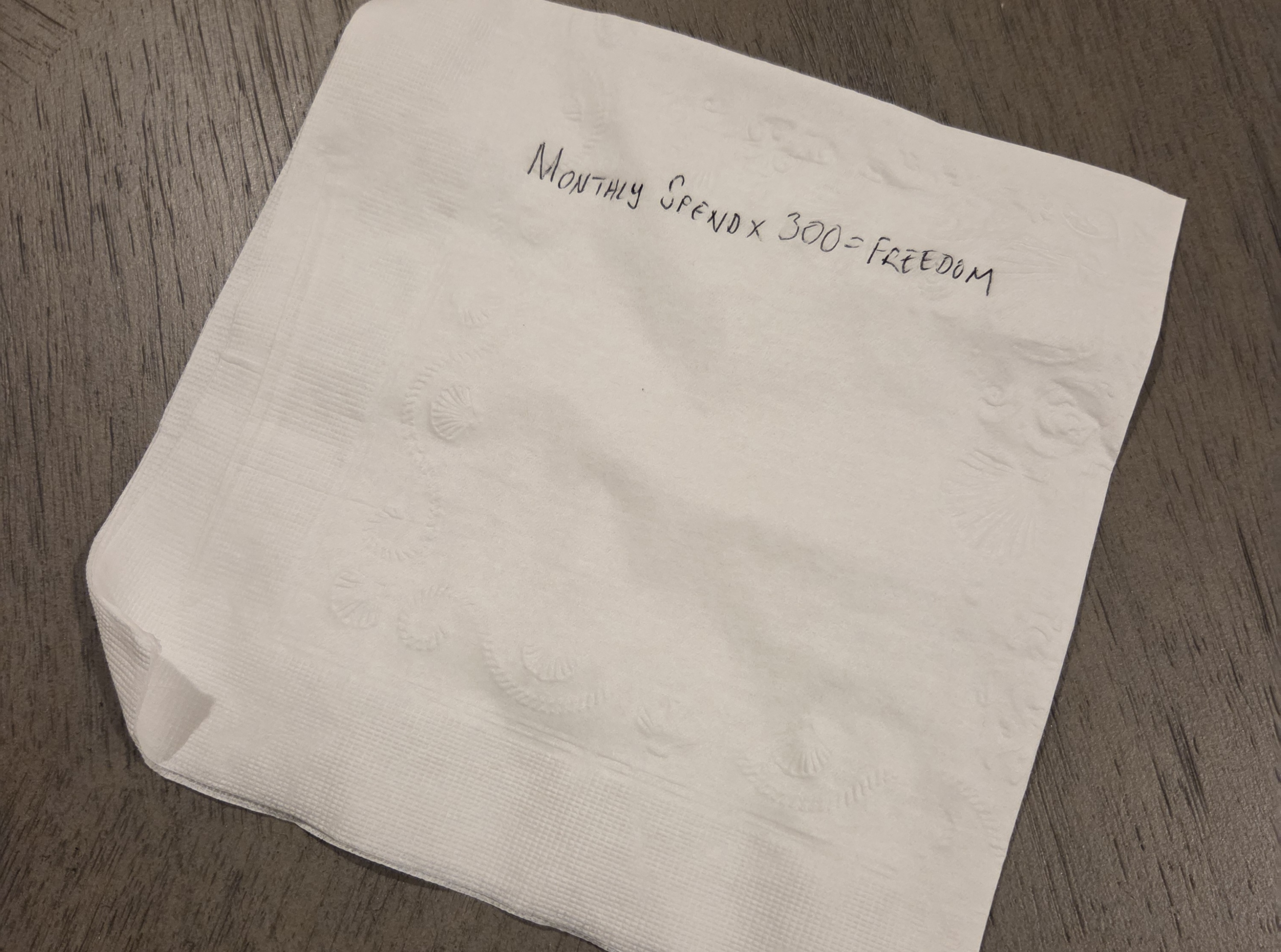

Stop agonizing over Monte Carlo simulations. Here is the simplest way to calculate your retirement number using the Rule of 25, plus a Javascript calculator to do the math for you.

Stop agonizing over Monte Carlo simulations. Here is the simplest way to calculate your retirement number using the Rule of 25, plus a Javascript calculator to do the math for you.

Deciding where to invest is just as important as deciding what to invest in. If you put money into your Brokerage account before maxing your 401(k) match, you are literally throwing away free money. If you max your 401(k) before paying off credit card debt, you are losing a guaranteed 20% return to pay for a potential 8% return. To build the 75% / 25% split efficiently, you need to follow the Financial Waterfall. You pour your income into the top bucket, and only when it overflows do you move to the next. ...

In the playground of personal finance, people love to argue about the “ultimate” investment account. “Roth is King!” screams the young influencer. “Defer taxes forever!” shouts the high earner. “Liquidity is power!” says the real estate investor. The truth is, investing is just a high-stakes game of Rock, Paper, Scissors. No account wins every time. Each one has a specific weakness that another account can exploit. Here is how the game is played, and how you can win by holding all three “throws” in your portfolio. ...

Is your life insurance policy acting as a safety net, or a drag on your financial freedom? For the vast majority of people building wealth, separating insurance from investment isn’t just a strategy—it’s a mathematical necessity. The Pitch vs. The Reality It’s a sales pitch almost everyone hears eventually: “Why rent your insurance when you can own it?” Agents position Whole Life insurance as a “swiss army knife” of finance—a product that offers death benefit protection, tax-advantaged savings, and a way to “bank on yourself.” It sounds perfect. It appeals to our desire for safety and efficiency. ...

Trying to increase your savings rate without giving too much up or burning the candle at both ends can be difficult. The goal isn’t to stop living; it’s to stop leaking money on things that don’t bring you value. Here are ten strategies—plus a bonus for parents—to keep an extra $1,000 (or more) in your pocket this year. 1. Stop Paying the “Lazy Tax” on Your Cash Most people leave their emergency fund in a standard checking or savings account earning 0.01%. This is a massive mistake. You need to move that cash to where it works for you, not the bank. ...

There is a common misconception that credit cards are purely tools for debt. If you treat them that way, they are. But if you treat them as tools for security and leverage, they are the first line of defense for your financial life. I don’t use debit cards. I don’t even carry one unless I am going to the ATM. Here is why I prefer using the bank’s money instead of my own. ...

Stop calculating your retirement taxes based on your current paycheck. This is the single most expensive math error high-earners make. It relies on a false assumption: that earning money and spending money are taxed the same way. They are not. Here is the breakdown of why earning $100,000 today is radically different than withdrawing $100,000 in retirement. The Earning Side: The “Top Dollar” Problem When you are working, every extra dollar you earn (or save) is taxed at your highest rate. This is your Marginal Rate. ...

Everyone loves the Roth IRA. It is the golden child of the personal finance world. “Pay taxes now,” they say, “so you never have to pay them again!” It sounds great emotionally. Mathematically, for the average engineer or professional, it is often a mistake. If you are earning $100,000, you are firmly in the 22% Federal Tax Bracket (plus state taxes). By choosing a Roth, you are volunteering to pay that 22% rate on money you don’t plan to touch for decades. ...